Understanding Net Worth: Calculate Yours & Build Wealth Today!

Ever wondered where you stand financially? Understanding your net worth is the crucial first step towards building a secure financial future, acting as a financial compass, guiding you towards your goals.

Net worth, at its core, is a snapshot of your financial health, a clear indicator of your assets versus your liabilities. It's a number that everyone should not only know but actively track. Knowing this number empowers you to make informed decisions about spending, saving, and investing, ultimately paving the way for a more prosperous future. Fortunately, numerous user-friendly, free tools are available to assist in calculating and monitoring your net worth regularly.

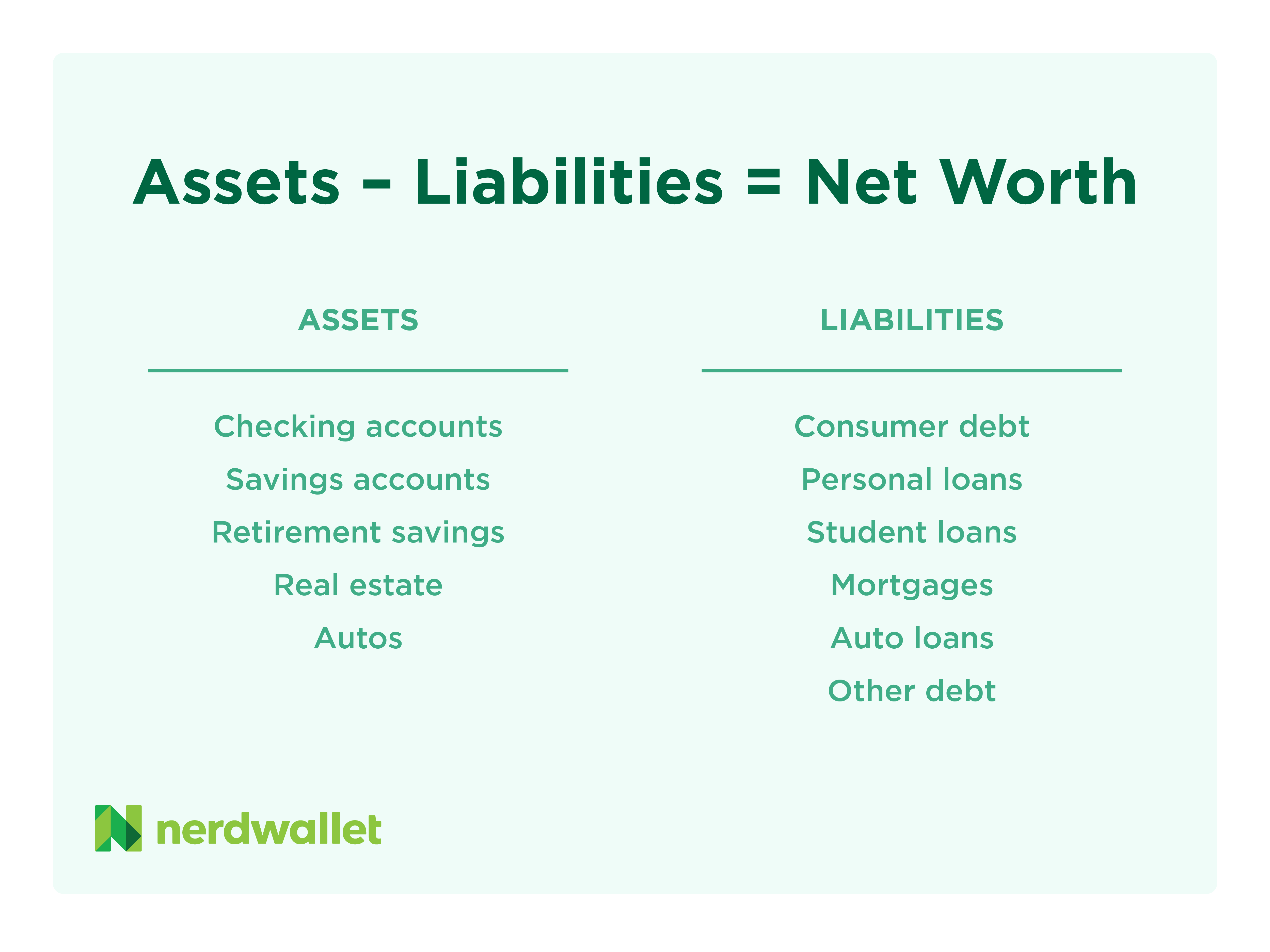

The concept of net worth is surprisingly straightforward: its what you own minus what you owe. Think of it as the financial equivalent of taking stock a personal balance sheet that reflects your true financial position. It's a fundamental concept applicable to individuals, businesses, and even entire countries. For individuals, it offers a clear picture of financial stability and progress toward long-term goals.

- Tiktok Fry99 Error No Results Found Heres Why

- Remote Raspberry Pi Access Ssh From Outside Your Network

Calculating your net worth is a simple yet powerful exercise. The formula itself is a fundamental equation: Total Assets Total Liabilities = Net Worth. However, to arrive at this figure, you'll need to meticulously list and value all your assets and liabilities. This process is more than just crunching numbers; its an opportunity to understand your financial strengths and weaknesses.

| Name | Whamos Vlogs |

| Channel Type | Film, Lifestyle, Entertainment |

| Nationality | Filipino |

| Subscribers (May 2, 2025) | 854,000+ |

| Videos Uploaded | 558 |

| Channel Start Date | Approximately 5 years ago (from May 2, 2025) |

| Estimated Net Worth (May 2, 2025) | To be determined (based on available data and estimations) |

| Reference | Whamos Vlogs YouTube Channel |

Let's break down each component. Assets are everything you own that has monetary value. This includes both liquid assets, like cash in your checking and savings accounts, and less liquid assets, such as real estate, investments (stocks, bonds, mutual funds), retirement accounts, vehicles, and valuable personal possessions. Accurately estimating the value of these assets is critical for an accurate net worth calculation. For real estate, a professional appraisal might be necessary. For investments, checking current market values is essential.

Liabilities, on the other hand, represent your debts and financial obligations. These include mortgages, student loans, auto loans, credit card debt, personal loans, and any other outstanding bills. Its crucial to include the outstanding balance on each of these liabilities, not just the monthly payment. Overlooking even small debts can skew your net worth calculation, painting an inaccurate picture of your financial health.

- Joyce Dewitts Net Worth From Threes Company To Millions

- Melissa Rauch Truth Behind The Leaked Photos Rumors

Once you have comprehensive lists of your assets and liabilities, the calculation is straightforward. Simply add up the total value of your assets and then add up the total value of your liabilities. Subtract your total liabilities from your total assets, and the result is your net worth. A positive number indicates that your assets exceed your liabilities, signifying a financially sound position. Conversely, a negative number indicates that you owe more than you own, a situation that requires careful attention and a plan to reduce debt and increase assets.

The interpretation of your net worth is highly personal and depends on various factors, including your age, income, lifestyle, and financial goals. However, generally speaking, a higher net worth indicates greater financial security and the ability to weather unexpected financial challenges. It also provides more opportunities to pursue your goals, such as retirement, homeownership, or starting a business.

For example, consider two individuals of the same age. One has a net worth of $100,000, primarily composed of savings and investments. The other has a net worth of -$50,000, due to significant student loan and credit card debt. The first individual is in a far stronger financial position, with more flexibility and options. They can afford to take more risks with their investments, knowing they have a safety net. They are also closer to achieving their long-term financial goals.

However, net worth should not be viewed in isolation. Its important to consider other financial metrics, such as income, expenses, and cash flow. Someone with a high income and low expenses can quickly improve their net worth, even if its currently negative. Conversely, someone with a high net worth but excessive spending habits may be heading for financial trouble.

The average net worth for U.S. families is approximately $1.06 million, according to recent data. However, this figure can be misleading due to the concentration of wealth at the top. A more representative measure is the median net worth, which is around $192,700. The median provides a more accurate reflection of the financial situation of the typical American family.

Its also important to consider the distribution of wealth across different age groups. Net worth typically increases with age, as individuals have more time to accumulate assets and pay down debt. For example, younger adults typically have lower net worths due to student loan debt and limited earning potential. As they progress in their careers and make smart financial decisions, their net worth tends to grow.

Setting financial goals is an essential part of managing your net worth. These goals should be specific, measurable, achievable, relevant, and time-bound (SMART). For example, a goal might be to increase your net worth by 10% in the next year or to pay off all credit card debt within six months. Having clearly defined goals provides motivation and helps you track your progress.

One of the most important benefits of tracking your net worth is that it allows you to identify areas where you can improve your financial situation. For example, if you have a high level of credit card debt, you can focus on paying it down. If you are not saving enough for retirement, you can increase your contributions to your retirement accounts. By monitoring your net worth, you can make informed decisions about how to allocate your resources.

Several strategies can help you boost your net worth. The most important is to increase your income and reduce your expenses. This can involve finding a higher-paying job, starting a side hustle, or simply cutting back on unnecessary spending. Another strategy is to invest your money wisely. This can involve investing in stocks, bonds, real estate, or other assets that have the potential to grow over time. Diversifying your investments is essential to reduce risk.

Another crucial factor is managing your debt effectively. High-interest debt, such as credit card debt, can quickly erode your net worth. Prioritizing paying down high-interest debt is essential. This can involve transferring balances to lower-interest cards, consolidating debt into a personal loan, or simply making extra payments each month.

Building and maintaining a positive net worth requires discipline, patience, and a long-term perspective. Its not a get-rich-quick scheme but a gradual process of accumulating assets and reducing liabilities. By tracking your net worth regularly, setting financial goals, and implementing smart financial strategies, you can build a secure and prosperous future.

Let's look at a couple of examples to illustrate the concept. Imagine Sarah, a 30-year-old professional with $50,000 in savings, $20,000 in investments, and a $200,000 mortgage on her home. Her assets total $270,000. She also has $10,000 in student loan debt and $5,000 in credit card debt, totaling $15,000 in liabilities. Sarah's net worth is $270,000 - $15,000 = $255,000. This positive net worth indicates a strong financial foundation.

Now consider David, a 25-year-old recent graduate with $5,000 in savings but $40,000 in student loan debt and $2,000 in credit card debt. His assets total $5,000, while his liabilities are $42,000. David's net worth is $5,000 - $42,000 = -$37,000. This negative net worth indicates a need to focus on debt reduction and asset accumulation.

Analyzing these examples highlights the importance of understanding and managing both assets and liabilities. While Sarah has a significant mortgage, her substantial savings and investments contribute to a healthy net worth. David, on the other hand, needs to prioritize paying down his student loan debt to improve his financial standing.

Consider Rebekah's situation. Her total assets amount to $29,925, while her liabilities reach $99,060, encompassing student loans, personal loans, auto loans, and credit card debt. Consequently, Rebekah has a negative net worth of $69,135. This situation highlights the burden of debt and the importance of developing a strategy to reduce liabilities and increase assets.

Achieving top-tier net worth status requires significant wealth accumulation. In 2025, individuals in the top 1% of net worth in the U.S. are projected to have $11.6 million or more. The top 2% will likely have a net worth of $2.7 million, and the top 5% will require $1.17 million. These figures demonstrate the substantial wealth required to be considered among the wealthiest Americans.

Aspiring to the top 25% requires a considerable net worth as well. While specific figures vary based on economic conditions and data sources, achieving this level of wealth requires consistent saving, investing, and sound financial management.

It's important to remember that net worth is not the only measure of financial success. Factors such as job satisfaction, work-life balance, and personal fulfillment also play a crucial role in overall well-being. However, understanding and managing your net worth is an essential step toward achieving financial security and pursuing your life goals.

Furthermore, net worth can be a valuable tool for evaluating your progress toward retirement. By estimating your future expenses and comparing them to your projected net worth at retirement age, you can determine whether you are on track to achieve your retirement goals. If not, you can make adjustments to your saving and investment strategies.

In conclusion, understanding and tracking your net worth is a fundamental aspect of personal financial management. It provides a clear snapshot of your financial health, allows you to set financial goals, and helps you identify areas where you can improve your financial situation. By actively managing your net worth, you can build a secure and prosperous future for yourself and your family.

Article Recommendations

- Aditi Mistry Scandal Leaks And Online Privacy The Truth

- Agency Reality Martins Divorce French Tv Show Drama More

Detail Author:

- Name : Dawson Cartwright

- Username : dboyer

- Email : allan74@gmail.com

- Birthdate : 1993-04-08

- Address : 629 Howell Pass South Bretttown, MT 44881

- Phone : (762) 230-9409

- Company : Steuber Inc

- Job : Farmworker

- Bio : Perspiciatis porro sint repellat iste. Facilis mollitia quia iusto error qui. Soluta id ullam maxime autem sed provident. Reprehenderit dolorum voluptatem id animi.

Socials

tiktok:

- url : https://tiktok.com/@rfranecki

- username : rfranecki

- bio : Minima sint quasi doloremque delectus. Sit et ut in quae sed facilis.

- followers : 4066

- following : 1518

twitter:

- url : https://twitter.com/russelfranecki

- username : russelfranecki

- bio : Quod enim enim inventore placeat tenetur et. Ut odio voluptas tempore et repellendus mollitia. Consequuntur placeat hic dolorum sint repellat.

- followers : 1593

- following : 1760